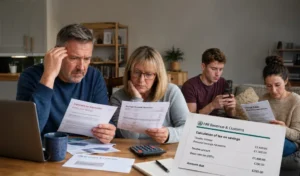

The HMRC savings tax error controversy has raised serious concerns for UK savers whose PAYE tax codes may have been changed using incorrect bank interest data.

Some savers have reportedly faced tax bills on interest they did not earn, duplicated figures, or even tax-free cash ISA interest. The main risk is that you could overpay before realising HMRC’s calculation is wrong.

Key Issues for Savers:

- HMRC uses bank and building society data to estimate savings tax.

- Errors can affect PAYE tax codes, salary, pension income, and tax bills.

- Cash ISA interest should not be taxed.

- You should check HMRC figures against your own bank records.

- Overpaid tax may be reclaimed if the calculation is corrected.

What Is Behind the HMRC Savings Tax Error and Why Are More UK Savers Being Affected?

The HMRC savings tax error appears to come from how savings interest data is reported and processed. Banks and building societies send interest figures to HMRC, which uses them to decide whether savers owe tax.

If the data is duplicated, outdated, wrongly matched, or incorrectly calculated, savers may face unexpected tax demands or PAYE tax code changes.

The Shift from Savings Tax Deductions to HMRC Data Reporting

Before the Personal Savings Allowance, tax was commonly deducted at source from savings interest. The newer system was designed to make savings tax simpler for most people, but it also moved responsibility into a data-driven process between banks and HMRC.

This means you may not personally report your savings interest, yet HMRC can still use reported figures to amend your tax code.

If those figures are duplicated, estimated wrongly, attached to the wrong year, or mixed with tax-free ISA interest, the error can flow straight into your tax calculation.

Why Frozen Allowances and Higher Interest Rates Are Widening the Impact?

Higher savings rates have pushed more people above the Personal Savings Allowance. At the same time, the allowance has not risen, meaning more ordinary savers are being drawn into the savings tax net.

Allowance snapshot:

| Taxpayer type | Personal Savings Allowance | Tax position on interest above allowance |

| Basic-rate taxpayer | £1,000 | Taxed at basic rate |

| Higher-rate taxpayer | £500 | Taxed at higher rate |

| Additional-rate taxpayer | £0 | All non-ISA savings interest taxable |

This matters because even a small reporting error can become expensive when HMRC adjusts your tax code based on incorrect savings income.

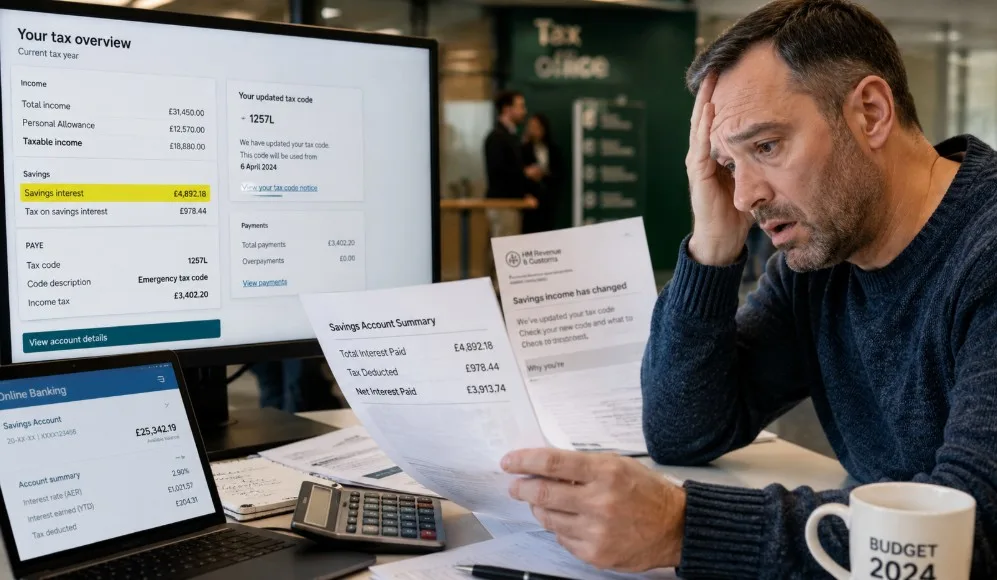

Why Are Some Savers Receiving Tax Bills for Interest They Never Earned?

Some savers are receiving tax bills because HMRC’s figures may not match their actual savings records. Interest can be estimated from old data, counted twice, placed in the wrong tax year, or linked to accounts the taxpayer does not recognise.

Robyn Lovatt, financial adviser at Shackleton, warned that savings interest estimates are being fed into tax codes “often without any clear breakdown of how the figures have been calculated”, adding that many taxpayers are left trying to catch up with estimated figures that may not reflect reality.

For PAYE taxpayers, the issue may only become clear when monthly pay drops, pension income changes, or a coding notice shows unexpected untaxed interest.

Common reported error types:

- Savings interest being duplicated in HMRC records.

- Cash ISA interest being treated as taxable.

- Previous tax year figures being used for the current year.

- Estimates replacing actual savings interest.

- Incorrect data being supplied or processed by financial institutions.

These issues can be difficult to spot unless you compare HMRC’s figures with your bank statements and tax notices.

How Does HMRC Use Bank and Building Society Data to Calculate Savings Tax?

HMRC receives savings interest data from banks and building societies and uses it to decide whether tax is due. For many PAYE taxpayers, this tax is collected by changing the tax code rather than asking them to complete a Self Assessment return.

The process is meant to be efficient, but it can create problems when data is incomplete or inaccurate.

How the process usually works:

| Stage | What happens | Risk for savers |

| Bank reporting | Banks report savings interest to HMRC | Figures may be wrong or misclassified |

| HMRC matching | HMRC links data to your tax record | Records may be duplicated or mismatched |

| Tax calculation | HMRC checks interest against your allowance | Estimates may not reflect reality |

| PAYE adjustment | Your tax code may be changed | Take-home pay may fall unexpectedly |

| Correction stage | You challenge the figure if wrong | You must provide evidence |

This system means you should not assume HMRC’s savings figure is automatically correct. Even when HMRC receives updated information later, the first tax code change may already have affected your income.

Could Your PAYE Tax Code Be Recovering Tax You Do Not Actually Owe?

Yes, it is possible. If HMRC believes you owe tax on savings interest, it can reduce your tax-free personal allowance through your PAYE code. That means your employer or pension provider deducts more tax from your pay or pension.

Common Signs Your Savings Figures May Be Incorrect

A wrong tax code does not always look obvious. Many taxpayers only realise something is wrong when their monthly income drops or when a coding notice includes savings interest they cannot explain.

Warning signs to watch:

- Your tax code changes without a clear reason.

- HMRC lists savings interest higher than your actual records.

- Your cash ISA appears to be included in taxable interest.

- Your pay or pension falls unexpectedly.

- HMRC uses an estimated figure instead of your actual bank interest.

“Sarah Weston, Technical Officer at the Low Incomes Tax Reform Group (LITRG), said there do appear to be instances where figures used by HMRC do not match taxpayers’ own records. She advised savers to check any savings interest figures shown in PAYE coding notices and end-of-year calculations rather than assuming they are automatically correct.”

Checking Tax Notices, Paye Codes and Bank Records

Start with your Personal Tax Account and your latest PAYE coding notice. Look for any line referring to untaxed interest, savings income or estimated interest. Then compare that figure with annual interest summaries from your banks and building societies.

You should also check whether the interest came from an ordinary savings account or a cash ISA. ISA interest should remain tax-free and should not be included in taxable savings income.

What Happens After HMRC Updates or Reverses a Calculation?

If HMRC accepts that the figure is wrong, it can amend your tax code. This may increase your take-home pay again and could trigger a refund if you have already overpaid.

However, corrections may not always happen instantly, especially where HMRC needs updated bank data or further evidence from you.

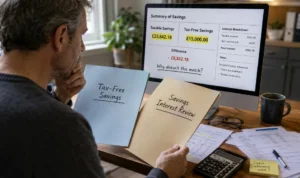

Are Cash ISAs and Other Tax-Free Savings Being Included by Mistake?

Cash ISA interest should not be taxed or counted towards your Personal Savings Allowance. If savings are held inside an ISA, the interest should not increase your tax bill.

Reports of cash ISA interest being wrongly included are concerning because these accounts are clearly designed to be tax-free. For savers, this can be confusing and may lead to incorrect tax code changes or overpayments.

Tax treatment comparison:

| Savings type | Is interest taxable? | Should it affect your Personal Savings Allowance? |

| Cash ISA | No | No |

| Stocks and shares ISA cash interest | Usually tax-free within ISA rules | No |

| Easy-access savings account | Yes, above allowance | Yes |

| Fixed-rate bond outside ISA | Yes, above allowance | Yes |

| Joint savings account outside ISA | Potentially, based on ownership share | Yes |

If HMRC’s figure appears to include ISA interest, you should challenge it and provide evidence from your ISA provider.

Who Faces the Greatest Risk from HMRC Savings Tax Errors?

Savers most at risk are those close to or above their Personal Savings Allowance. With higher interest rates, ordinary savings accounts can now generate enough interest to trigger tax, even for people who never paid savings tax before.

Basic-rate taxpayers can earn up to £1,000 tax-free, higher-rate taxpayers get £500, and additional-rate taxpayers receive no Personal Savings Allowance.

More exposed groups include:

- PAYE workers with multiple savings accounts

- Pensioners with taxable pension income

- Higher-rate taxpayers

- Joint account holders

- Savers with both ISA and non-ISA accounts

This matters because more savers are now affected by HMRC’s data-driven system.

What Should You Do If You Think HMRC Has Calculated Your Savings Tax Incorrectly?

If you think HMRC has calculated your savings tax incorrectly, act quickly. An incorrect tax code can keep reducing your pay or pension income until the issue is fixed. The aim is to check the figures, collect evidence and ask HMRC to explain or amend the savings interest amount.

Practical action checklist:

- Check your PAYE coding notice to see the savings figure used

- Log in to your Personal Tax Account to review your tax code

- Collect bank interest certificates or annual statements

- Separate ISA interest from taxable non-ISA savings interest

- Contact HMRC with clear evidence and request a correction

- Keep records of calls, letters and reference numbers

Do not ignore a coding notice, even if the amount seems small. Estimated figures can affect current and future tax calculations.

Will Future HMRC Reporting Rules Reduce Errors or Create More Concerns for Savers?

Future reporting changes are intended to improve accuracy by giving HMRC more frequent and detailed savings information. Reports suggest banks may be required to collect National Insurance numbers from customers and provide savings data more regularly.

In theory, this could reduce matching errors and help HMRC calculate tax more accurately. In practice, it also raises concerns about privacy, data quality and whether more automated reporting could create more automated mistakes.

For savers, the key lesson is simple: greater data sharing does not remove the need to check your own records. The system may become faster, but speed is not the same as accuracy.

Conclusion

The HMRC savings tax error shows why savers should not automatically trust every tax code change. Bank data can be duplicated, outdated, wrongly matched, or incorrectly classified.

To avoid overpaying, check your tax code, compare HMRC’s savings figure with your own records, and challenge anything that looks wrong.

Cash ISA interest should not be taxed, and savings interest should only be taxed when it exceeds the relevant allowance. Your records remain your strongest protection

FAQs About HMRC Savings Tax Error

Why might HMRC use estimated savings interest?

HMRC may use previous bank data or recent information from financial institutions to estimate your current year’s savings interest. This can cause problems if your savings balance or interest rate has changed.

Can a joint savings account cause a tax mismatch?

Yes, joint accounts can create confusion if interest is not split correctly between account holders. You should check whether HMRC has attributed the correct share to you.

Does a cash ISA count towards your Personal Savings Allowance?

No, cash ISA interest is tax-free and does not use up your Personal Savings Allowance. If it appears as taxable savings income, you should query it.

Can an HMRC savings mistake affect pensioners?

Yes, pensioners can be affected if HMRC adjusts the tax code applied to their pension income. This can reduce pension payments until the code is corrected.

Will HMRC automatically refund overpaid savings tax?

Not always immediately. HMRC may refund overpaid tax after correcting its records, but you should contact them if you believe the repayment has not been processed.

What records should you keep for savings tax checks?

You should keep annual interest summaries, bank statements, ISA statements, PAYE coding notices and any HMRC tax calculations for the relevant tax year.

Can you complain if HMRC does not correct the error?

Yes, you can use HMRC’s complaints process if the issue is not resolved. If the matter remains unresolved, you may be able to escalate it through the appropriate complaints channels.